The Great Ponzi Shakedowns: Bart Henderson

Lambs to the Slaughter

What We Have Here Is a Failure to Investigate

Under South Africa’s four pillars of regulatory oversight for financial investments, why do so many fraudsters appear to escape accountability for years?

The answer is uncomfortable but simple: too often, nobody is actively looking for fraud. In many cases, nobody wants to look. Some are too busy profiting from the system to question it. Others, it seems, are paid to look away.

The people behind major fraud schemes are rarely as unique as they imagine. There is a recognisable type. They believe they are the smartest person in the room. They believe the rules do not apply to them. They believe they will never be caught. And, for a time, they usually are right.

A defining trait in many of these cases is a form of sociopathy in which profit eclipses empathy, morality, and social responsibility. People become instruments for extraction. Manipulation becomes business practice. Human damage becomes collateral.

In the case of the BHI Trust Ponzi scheme, one figure appears to embody that ethos particularly strongly, and it is not Craig Warriner, who is now serving a 25-year prison sentence.

Every Ponzi scheme has its own cast of characters, structures, and methods. Each also produces its own pattern of regulatory response, or lack of response. If South Africa is to learn anything from these scandals, beyond the devastation they inflict on victims and the reputational damage they cause to the country, it must confront the regulatory failures and oversight gaps that allowed them to flourish in the first place.

Regulatory Oversight of Financial Investments in South Africa

South Africa’s financial sector is regulated under the Twin Peaks framework, established by the Financial Sector Regulation Act, 2017. This framework divides responsibility between two regulators:

-

The Prudential Authority (PA), responsible for safety and soundness

-

The Financial Sector Conduct Authority (FSCA), responsible for market conduct and investor protection

These regulators operate alongside key legislation such as the FAIS Act, CISCA, and prudential standards governing collective investment schemes, intermediaries, and financial advice.

The four pillars of effective regulatory oversight are:

1. Licensing

Gatekeeping to ensure only fit-and-proper entities and individuals operate in the financial sector.

2. Regulatory Requirements

Setting standards, prudential rules, and conduct requirements.

3. Supervision

Ongoing monitoring, inspections, and risk-based oversight.

4. Enforcement

Taking remedial, punitive, or corrective action where breaches occur.

Alongside Twin Peaks sits FICA, the Financial Intelligence Centre Act, 2001, which forms South Africa’s anti-money laundering and counter-terrorist financing regime. FICA is enforced by the Financial Intelligence Centre (FIC) and applies to accountable institutions such as advisers, brokers, and collective investment managers.

In theory, this framework should create a strong defense against fraud, misconduct, and money laundering. In practice, however, several of South Africa’s largest Ponzi schemes reveal how weak enforcement, delayed action, and fragmented oversight can render the framework ineffective.

South Africa’s Biggest Ponzi Schemes and Oversight Failures

1. Mirror Trading International (MTI) – Johann Steynberg (2018–2021)

Mirror Trading International became South Africa’s largest crypto Ponzi scheme, reportedly involving around R30 billion in Bitcoin and more than 280,000 victims. The scheme appears to have evaded meaningful intervention for roughly two years through a mix of technological opacity, regulatory uncertainty around crypto assets, and multi-level marketing recruitment.

The first major detection point did not come from local regulators. It came from FXChoice, a Belize-based broker, which in July 2020 demanded audited financial statements after participant complaints. MTI refused. FXChoice then reportedly flagged the account as fraudulent and froze approximately 1,280 BTC on 7 August 2020.

Only after that did the FSCA begin investigating. Public warnings followed in August 2020, premises were raided in October, and in December 2020 the FSCA said MTI had been conducting an illegal operation and misleading clients.

2. Barry Tannenbaum Pharma Import Scheme (2005–2009)

The Barry Tannenbaum fraud, estimated at R12.5 billion, was presented as an investment in pharmaceutical active ingredients for ARV drugs. Investors were shown forged documentation and promised returns of up to 200% per year.

The scheme appears to have operated for several years without any proper licensing under the FAIS Act or any collective investment authorization. Despite red flags, oversight bodies did not intervene proactively. Banks filed suspicious transaction reports, including one by Rand Merchant Bank in 2007, but no visible enforcement action followed.

The case later became one of the examples used to justify strengthening investor protection under the FAIS framework.

3. Louis Liebenberg / Tariomix / Forever Diamonds & Gold (2019–2024 and beyond)

The Louis Liebenberg diamond investment scheme allegedly raised R4 billion to R4.5 billion from thousands of investors through social media-driven recruitment and promises of returns exceeding 100%.

The operation appears to have run for years without licensing or registration. A Hawks and NPA investigation reportedly began as early as 2019. A Carte Blanche exposé aired in 2020. Assets were frozen in 2021. Yet arrests only followed in October 2024.

That delay matters. It may have allowed further fundraising and greater losses long after serious concerns had been raised publicly and within law enforcement channels.

4. BHI Trust – Craig Warriner (2008–2023/2024)

The BHI Trust scandal has become one of South Africa’s most disturbing examples of a long-running, high-trust Ponzi scheme. It reportedly raised R2.9 billion from around 800 victims, many of them retirees, through promises of steady annual returns above 10%.

According to the FSCA’s own findings, only around 20% of investor funds were placed in legitimate investments. The remaining 80% allegedly sat in a Nedbank money market account and was used to pay earlier investors while also funding Craig Warriner’s lifestyle.

The scheme appears to have operated for roughly 15 years, despite multiple red flags, reports, and complaints.

The BHI Trust Case and FSCA’s Failure to Act

A central question hangs over the BHI Trust matter:

Why did the FSCA take from 2013 until 17 August 2023 to serve Global and Local and Michael Haldane with a Notice of Intended Administrative Action?

This is not a minor procedural delay. It is the heart of the regulatory failure.

The case was serious enough for the FSCA to eventually debar Michael Haldane and Mauro Forlin for 30 years, and to withdraw Global and Local’s licence. Yet those steps came years after warnings had reportedly been raised.

One part of the FSCA’s own reasoning is especially striking. Paragraph 3.2.3 of the final report reportedly considered:

“any loss or damage suffered by any person as a result of the conduct”

and concluded:

“There have been no losses suffered by clients thus far.”

The BHI Trust collapsed barely a month later, with estimated losses exceeding R1.9 billion.

If that paragraph influenced the absence of a financial penalty against Haldane and Forlin at the time, then timing appears to have spared them a far harsher outcome. That is difficult to justify, especially given the length of the investigation and the scale of the eventual losses.

By the time Michael Haldane was debarred on 20 September 2024, the damage was no longer theoretical. It was obvious. The FSCA had months in which investor losses were publicly known, yet no additional fines appear to have followed.

The result is a troubling impression: that justice was delayed, diluted, and ultimately denied.

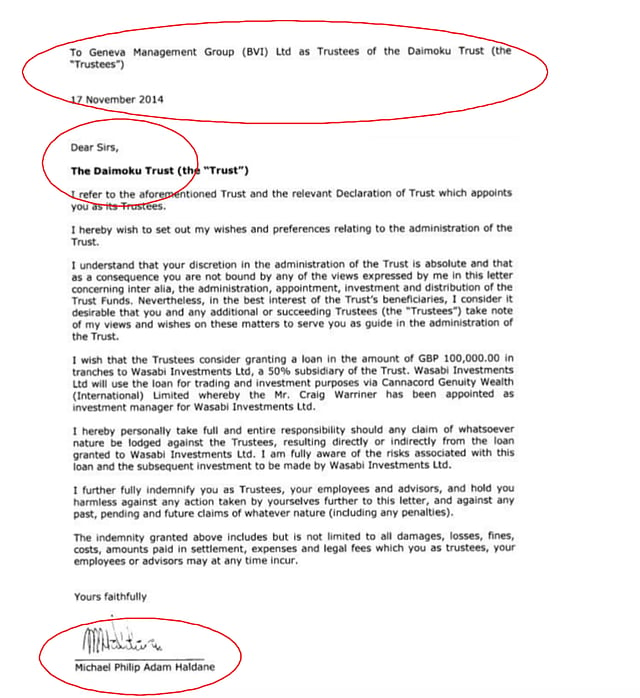

The Devil in the Detail: Amalgum 108 and the BHI Plus Strategy

One paragraph in the FSCA investigation report stands out as particularly important. In paragraph 3.7 of the FSCA Investigation Report: BHI Trust, Global & Local Investment Advisors (Pty) Ltd, Rubicon Administration Services (Pty) Ltd and Mr Craig Roy Warriner, dated 17 April 2023, the report states:

“On 6 February 2013, the relationship between Axiam and BHI Trust was terminated. After this termination, Warriner remained a representative of Axiam and managed another client’s portfolio known as ‘Amalgum’, which was not a subject of this investigation.”

That exclusion may be one of the most consequential omissions in the entire BHI matter.

If Amalgum 108 was in fact part of the BHI Plus Strategy, then excluding it from the investigation may have cut investigators off from a key money trail, a key ownership trail, and a key structural link in the alleged fraud.

This is not a technical footnote. It may be the lynchpin.

Why Amalgum 108 Matters

Amalgum 108 appears, based on the records cited, to have played a central role in the movement and extraction of investor funds. Its exclusion from the FSCA investigation may have shaped the terms of reference for other agencies, including the SAPS, the NPA, and the DPCI, potentially limiting the scope of follow-up investigations.

If that happened, the consequences were enormous.

According to the argument made by the documentary trail cited here, Amalgum 108 was tied to the BHI Plus strategy, offshore entities, dividend flows, and ownership structures that may identify who really controlled and benefited from much of the scheme.

Craig Warriner has pleaded guilty, been convicted, and is serving a prison sentence. But the documentary evidence described here argues that he did not act alone, and may not have been the ultimate beneficiary.

That raises a critical question:

Why were charges against Michael Haldane and Sona Pillay reportedly provisionally withdrawn?

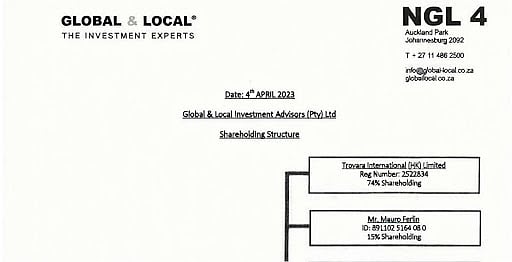

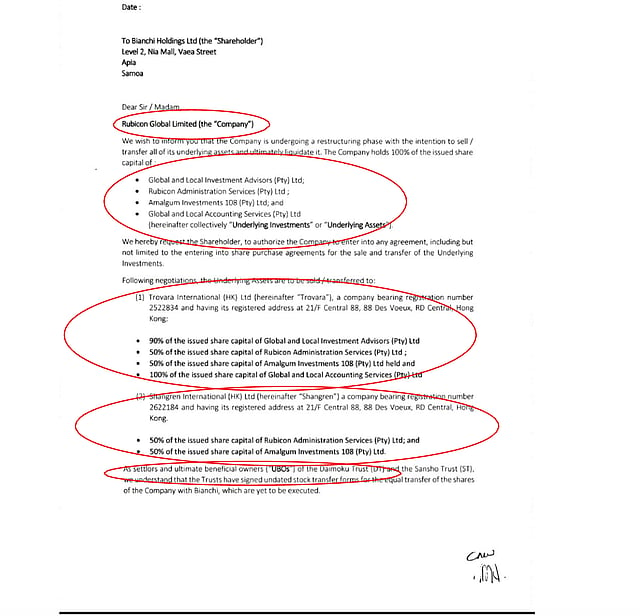

The Ownership Trail: Global and Local, Amalgum 108, and Offshore Structures

The records cited suggest the following pattern:

-

Trovara International HK Limited reportedly held 74% of Global and Local

-

Trovara and Shangren, both Hong Kong-linked entities, reportedly held 100% of Amalgum 108

-

Rubicon Global Limited previously held 100% of Global and Local

-

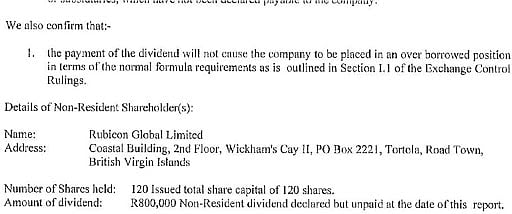

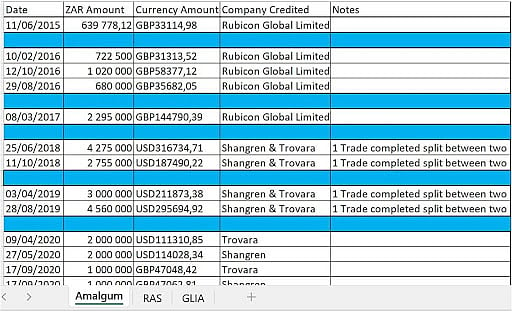

Dividend certificates and spreadsheets reportedly show significant offshore flows involving Rubicon Global, Trovara, Shangren, Amalgum 108, Rubicon Administration, and Global and Local

If accurate, these records suggest overlapping ownership, control, and financial benefit across the adviser, fund structures, and administrative machinery surrounding BHI.

That would mean the entities referring investors into BHI may also have been financially benefiting from the same underlying structures in multiple ways.

At minimum, that presents a major conflict of interest.

At worst, it may suggest an integrated extraction mechanism hidden behind advisory, administrative, and offshore vehicles.

Double Dipping, Triple Dipping, and Fake Performance Statements

According to the evidence described, Rubicon Administration had responsibility for producing investor statements. Those statements allegedly reflected fictitious returns. If so, they did not merely mislead investors; they may have helped sustain the fraud by creating the appearance of legitimate performance.

At the same time, the structure described suggests that fees and commissions may have been drawn from several connected sources:

-

Global and Local as adviser

-

BHI Trust as investment strategy

-

Amalgum 108 / BHI Plus as investment vehicle

-

Rubicon Administration as administrator

This is described as a form of double dipping, or even triple dipping. Whether every layer of that structure was independently unlawful is one question. Whether the full structure was properly disclosed, supervised, and scrutinized is another.

That second question is the more important one.

Because where there are undisclosed conflicts of interest, misleading omissions, fictitious statements, and connected-party benefit, the risk to investors becomes extreme.

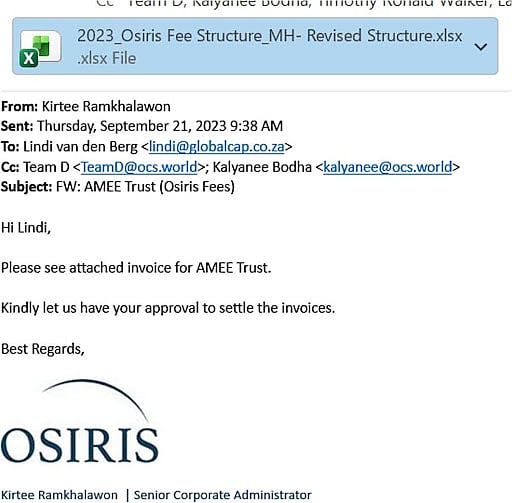

The Offshore Restructuring Question

The records also point to offshore trust and corporate structures involving:

-

AMEE Trust

-

Emieri Trust

-

Trovara (HK)

-

Shangren (HK)

-

Mauritius and British Virgin Islands structures

-

An email exchange titled “MH Revised Structure”

The timing of this alleged restructuring is especially important. It reportedly occurred in late September 2023, shortly after the FSCA’s 17 August 2023 notice of intended administrative action and shortly before the scheme was formally reported to police in October 2023.

That timing raises obvious questions.

If assets were being restructured offshore while regulatory pressure was increasing and the scheme was approaching collapse, investigators should have been all over it.

What the Documentary Record Appears to Show

Based on the material cited, the article’s core argument is this:

-

The FSCA identified three BHI strategies: BHI, BHI Plus, and BHI International

-

But there is no clear public record showing a full investigation into BHI Plus / Amalgum 108 or BHI International

-

Following the Amalgum trail may reveal ownership, beneficial control, and fund flows well beyond Craig Warriner

-

The records suggest Michael Haldane may have held a central role in the structure, control, and financial benefit associated with the scheme

-

The omission of Amalgum 108 from the FSCA investigation may have compromised the broader pursuit of accountability

If that reading is correct, then Craig Warriner may have been the visible operator, but not the sole architect or ultimate beneficiary.

A Failure of the Twin Peaks Framework

The BHI Trust matter appears, on this account, to represent a systemic failure of South Africa’s regulatory architecture.

The Twin Peaks model is designed to ensure licensing, rule-making, supervision, and enforcement. FICA is meant to help detect suspicious financial flows and reduce money laundering risk. Yet in this case:

-

warnings were allegedly ignored

-

investigations were delayed

-

a key component was allegedly excluded from scrutiny

-

losses multiplied over years

-

victims were left without meaningful restitution

-

broader accountability appears incomplete

That is not merely a failure of process. It is a failure of public protection.

Unanswered Questions for the FSCA, NPA, and DPCI

The documentary record described here raises serious questions for:

-

Unathi Kamlana, FSCA

-

Advocate Andy Mothibi, NPA

-

Lieutenant General Siphesihle “ST” Nkosi, DPCI

At face value, the records appear to warrant far deeper scrutiny into:

-

the exclusion of Amalgum 108 from the BHI investigation

-

the absence of timely fines against key individuals

-

the provisional withdrawal of criminal charges

-

the tracing of offshore fund flows

-

the full ownership and beneficial interest behind Trovara, Shangren, Rubicon, and related entities

-

the role of connected advisers and administrators in sustaining the scheme

Victims deserve more than a single high-profile conviction. They deserve a full accounting of who benefited, who enabled the conduct, who failed to act, and whether stolen funds can still be traced and recovered.

Conclusion: Justice Requires More Than One Conviction

Craig Warriner’s conviction may have closed one chapter of the BHI Trust saga, but it does not appear to close the case.

If the records discussed here are accurate, then the BHI Trust scandal is not simply the story of a lone Ponzi operator. It is the story of a wider structure involving financial advisers, administrators, offshore entities, alleged conflicts of interest, delayed regulatory intervention, and glaring investigative omissions.

That is why the exclusion of Amalgum 108 matters.

That is why the FSCA’s delay matters.

That is why the provisional withdrawal of charges matters.

And that is why South Africans should care. Because if fraud on this scale can operate for years inside a heavily regulated environment, despite tip-offs, complaints, and documentation, then the problem is not only the fraudsters.

It is the system that failed to stop them.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}